The Fundamental Difference

All three are life insurance products, but they serve very different purposes:

- Term Insurance: Pure protection. Pay premium → Get death cover. No maturity benefit.

- Endowment Plan: Protection + Guaranteed Savings. Pay premium → Get death cover + guaranteed maturity amount.

- ULIP: Protection + Market-Linked Investment. Pay premium → Get death cover + market-based returns.

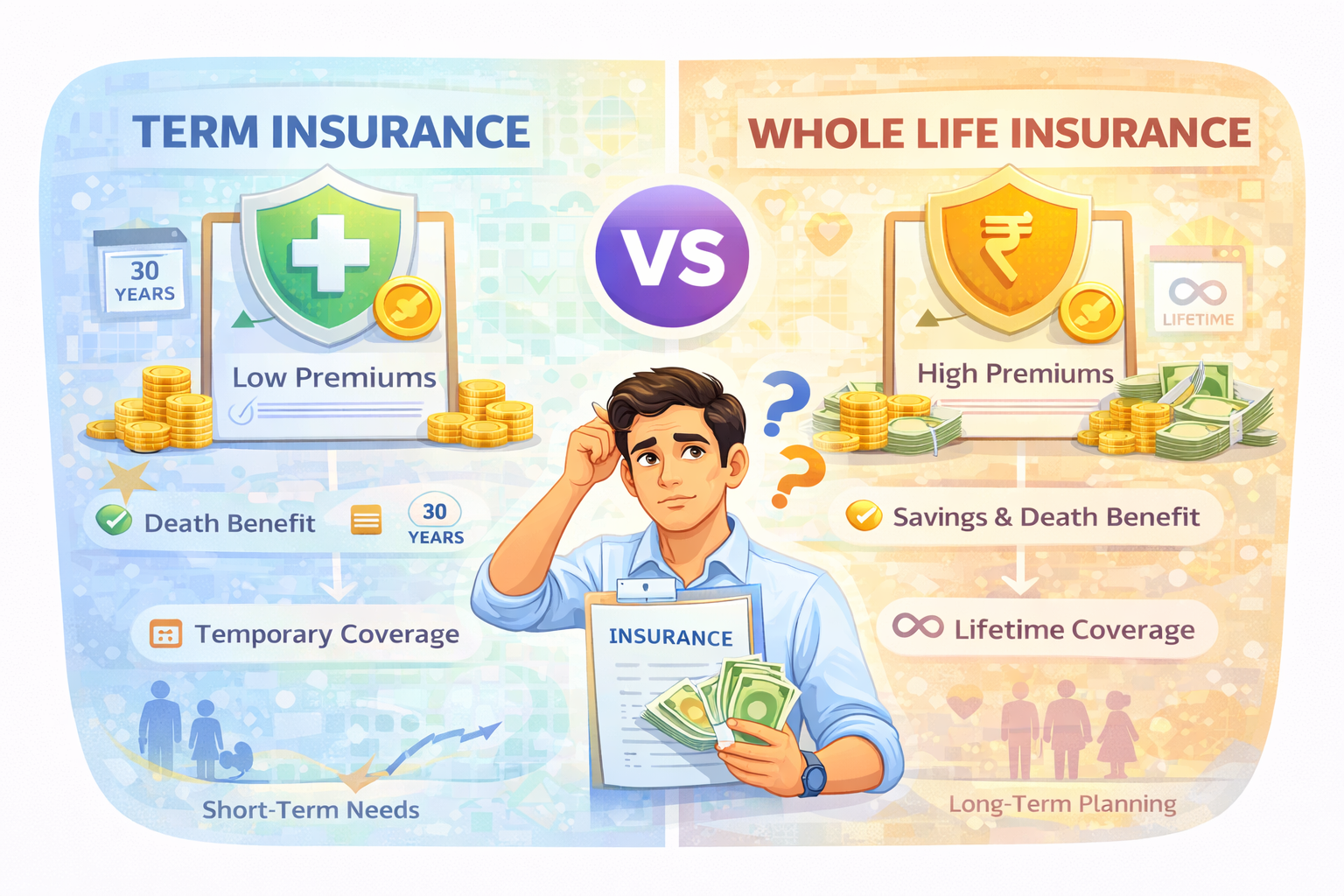

Term Insurance — Maximum Coverage at Minimum Cost

How it Works

You pay a fixed premium for a specific term (10-40 years). If you die during the term, your family gets the sum assured (₹50 lakhs, ₹1 crore, etc.). If you survive, you get nothing back.

Example

30-year-old male, ₹1 Crore cover for 30 years

Annual Premium: ₹12,000–15,000/year

Total Paid in 30 years: ₹4.5 lakhs

Death Benefit: ₹1 Crore (tax-free to family)

Maturity Benefit: ₹0 (if you survive)

Pros

- Highest coverage for lowest premium

- Pure protection for family

- Tax benefits under Section 80C (premium) and 10(10D) (claim)

- Simple, transparent, no hidden charges

Cons

- No maturity benefit — feels like "money wasted" if you survive

- No savings/investment component

Best For

- Anyone with financial dependents (spouse, children, parents)

- Primary breadwinner of the family

- Young professionals starting their career

- People who want maximum coverage at lowest cost

Endowment Plan — Guaranteed Returns but Low Coverage

How it Works

You pay premium for 10-20 years. Insurer invests your money in debt instruments (bonds, FDs). After maturity, you get guaranteed sum assured + bonuses. If you die during the term, family gets sum assured.

Example

30-year-old, ₹10 lakh endowment plan for 20 years

Annual Premium: ₹45,000/year

Total Paid in 20 years: ₹9 lakhs

Maturity Amount (approx): ₹12-13 lakhs (bonuses included)

Effective Returns: 4-5% per year (barely beats inflation)

Death Benefit: ₹10 lakhs only

Pros

- Guaranteed maturity benefit (you get money back)

- Forced savings discipline

- Safe, no market risk

- Tax benefits under Section 80C

Cons

- Very low coverage (₹10L cover for ₹45K premium vs ₹1Cr cover for ₹12K in term)

- Poor returns (4-5% vs 10-12% in mutual funds)

- High charges and commissions eat into returns

- Locks your money for 15-20 years with poor liquidity

Best For

- Ultra-conservative investors who cannot stomach market volatility

- People with no financial discipline (need forced savings)

- Senior citizens looking for guaranteed income (annuity plans)

Our Take

NOT recommended for wealth creation. Returns are poor. Better strategy: Buy term insurance + invest in mutual funds separately.

ULIP — Market-Linked Returns with Insurance

How it Works

Premium is split into two parts: small portion for insurance, majority invested in equity/debt funds. Returns depend on market performance. Lock-in period of 5 years.

Example

30-year-old, ₹2 lakh/year ULIP for 10 years

Total Investment: ₹20 lakhs

Life Cover: ₹20-25 lakhs (10-12.5x of premium)

Maturity Value (assumed 10% returns): ₹32-35 lakhs after 10 years

Effective Returns: 8-12% depending on fund performance

Charges in ULIPs

- Premium Allocation Charge: 2-7% (deducted upfront)

- Policy Administration Charge: ₹300-500/month

- Fund Management Charge: 1-1.5% per year

- Mortality Charge: Cost of life cover (increases with age)

- Surrender Charge: If you exit before 5 years

Pros

- Market-linked returns (better than endowment)

- Flexibility to switch between equity/debt funds

- Life cover included

- Tax-free maturity under Section 10(10D)

- 5-year lock-in ensures discipline

Cons

- High charges (especially in first 5 years)

- Low life cover compared to term insurance

- Returns depend on market — not guaranteed

- Complex product, difficult to understand

- Better to separate insurance and investment

Best For

- High-income individuals looking for tax-free long-term returns

- People who want market exposure but need forced discipline

- HNIs exhausting 80C limit (ULIP has no upper limit for tax-free maturity)

Side-by-Side Comparison

| Feature | Term Insurance | Endowment | ULIP |

|---|---|---|---|

| Primary Purpose | Pure Protection | Savings + Protection | Investment + Protection |

| Premium (for ₹10L cover) | ₹1,200/year | ₹45,000/year | ₹20,000/year |

| Returns | None (if survive) | 4-5% guaranteed | 8-12% market-linked |

| Maturity Benefit | ₹0 | ₹12-13L (after 20 years) | ₹32-35L (if 10% returns for 10 years) |

| Risk | Zero (pure insurance) | Zero (guaranteed) | Market Risk |

| Transparency | Very High | Low | Medium |

| Charges | Very Low | High (hidden) | High (disclosed) |

The Smart Strategy: Term + Mutual Funds

Instead of ULIP or endowment, financial planners recommend:

- Buy Term Insurance for maximum coverage (₹1 Cr for ₹12,000/year)

- Invest the difference in mutual funds via SIP (₹3,000/month in good equity fund)

Result after 20 years:

- Life Cover: ₹1 Crore (term insurance)

- Investment Corpus: ₹25-30 lakhs (SIP at 12% returns)

- Total Premium Paid: ₹2.4 lakhs (term) + ₹7.2 lakhs (SIP) = ₹9.6 lakhs

vs Endowment (₹45,000/year):

- Life Cover: ₹10 lakhs only

- Maturity Amount: ₹12-13 lakhs

- Total Premium Paid: ₹9 lakhs

Winner: Term + MF gives 10x life cover + 2x wealth creation for the same outflow!

Final Recommendation

- For Protection: Always buy Term Insurance. No debate.

- For Savings: Skip endowment. Returns are terrible.

- For Investment: ULIPs can work for high-income tax payers, but mutual funds are better for most people.

- Best Strategy: Term Insurance (for protection) + Mutual Fund SIP (for wealth creation)

Need help choosing the right life insurance? Connect with our experts for personalized recommendations.